Wondering how much salary is needed to buy a villa in Hyderabad? Learn home loan eligibility, down payment requirements, and smart financial planning tips.

There is something special about owning a villa in Hyderabad.

Maybe it’s the idea of waking up in your own private space instead of hearing your neighbor’s pressure cooker whistle through a shared apartment wall. Or perhaps it’s the dream of having a garden, a terrace, and enough parking space that doesn’t require advanced-level driving skills.

Whatever your reason, one question usually comes first:

“How much salary do I actually need to buy a villa in Hyderabad?”

If you’re a young IT professional, entrepreneur, or salaried employee, you’ve probably wondered whether a villa is realistically within reach.

The good news? It may be more achievable than you think.

In this guide, I’ll break down the salary required to buy a villa in Hyderabad, home loan eligibility, down payment requirements, and practical financial planning tips that can help you move from dreaming about a villa to actually owning one.

Understanding Villa Prices in Hyderabad

Before discussing salary requirements, let’s look at current villa pricing trends.

Hyderabad has become one of India’s fastest-growing real estate markets. Areas like Tellapur, Kollur, Mokila, Patancheru, Kompally, Shamirpet, and Adibatla have witnessed significant villa development over the past few years.

Average Villa Prices in Hyderabad

| Villa Category | Approximate Price Range |

| Entry-Level Villas | ₹75 Lakhs – ₹1 Crore |

| Mid-Range Villas | ₹1 Crore – ₹1.5 Crores |

| Premium Villas | ₹1.5 Crores – ₹2.5 Crores |

| Luxury Villas | ₹2.5 Crores+ |

Many reputed developers currently offer villas starting around ₹75 Lakhs and extending beyond ₹2 Crores depending on location, amenities, and project specifications.

This is where salary becomes an important factor.

What Salary Is Required to Buy a Villa in Hyderabad?

Banks generally prefer your total EMI obligations to stay within 40%–50% of your monthly income.

Let’s simplify that.

If your salary is ₹1 lakh per month, lenders usually feel comfortable if your home loan EMI remains around ₹40,000 to ₹50,000.

Estimated Salary vs Villa Budget

| Monthly Salary | Approx Loan Eligibility | Villa Budget (with Down Payment) |

| ₹75,000 | ₹35–40 Lakhs | ₹45–50 Lakhs |

| ₹1 Lakh | ₹50–60 Lakhs | ₹65–75 Lakhs |

| ₹1.5 Lakhs | ₹80–90 Lakhs | ₹1–1.1 Crores |

| ₹2 Lakhs | ₹1–1.2 Crores | ₹1.25–1.5 Crores |

| ₹3 Lakhs | ₹1.5–1.8 Crores | ₹2 Crores+ |

These figures may vary based on:

- Existing loans

- Credit score

- Employment stability

- Age

- Loan tenure

- Bank policies

So, when people ask about the income needed for villa purchase in Hyderabad, the answer depends on the villa price and your financial profile.

Can I Buy a Villa in Hyderabad with a Salary of ₹1 Lakh Per Month?

This is one of the most common questions among young professionals.

The answer is: Yes, but with careful planning.

Let’s assume:

- Monthly salary: ₹1 lakh

- Home loan tenure: 25 years

- Interest rate: 8.5%

- EMI affordability: ₹45,000–₹50,000

Under these conditions, you may qualify for a home loan of around ₹50–60 lakhs.

If you can contribute a substantial down payment, say ₹15–20 lakhs or more, buying a villa priced around ₹70–80 lakhs become possible.

Many first-time buyers achieve this through:

- Personal savings

- Performance bonuses

- ESOP payouts

- Joint applications with spouses

Think of it like building a cricket team. Your salary is the captain, but your savings and down payment are the all-rounders that strengthen the squad.

How Much Home Loan Can I Get Based on My Salary?

Banks generally calculate home loan eligibility using:

1. Monthly Income

Higher income usually means higher eligibility.

2. Existing Financial Commitments

If you’re paying:

- Car loans

- Personal loans

- Credit card EMIs

Your loan eligibility may reduce.

3. Credit Score

A score above 750 improves approval chances and may help secure better interest rates.

Home Loan Eligibility Estimate

| Monthly Salary | Potential Loan Eligibility |

| ₹1 Lakh | ₹50–60 Lakhs |

| ₹1.5 Lakhs | ₹80–90 Lakhs |

| ₹2 Lakhs | ₹1–1.2 Crores |

| ₹3 Lakhs | ₹1.5–1.8 Crores |

Always remember that loan eligibility is not the same as affordability.

Just because a bank offers a larger loan doesn’t mean you should stretch your finances to the limit.

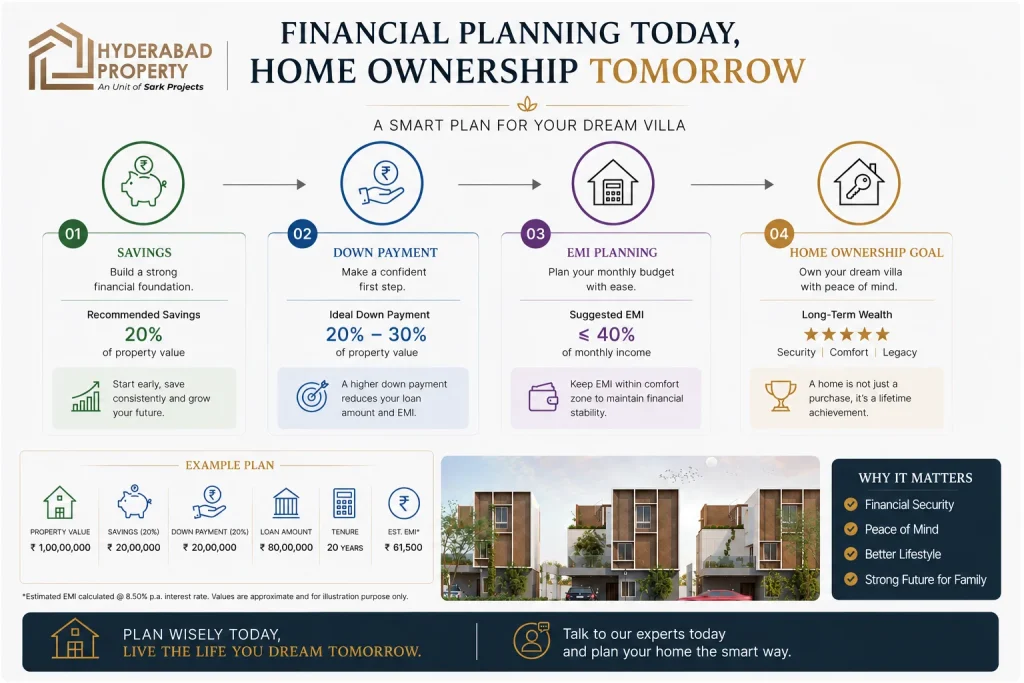

What Is the Ideal Down Payment for Buying a Villa in Hyderabad?

Most banks finance 75% to 80% of the property value.

This means you’ll need to arrange the remaining amount as a down payment.

Recommended Down Payment Structure

| Villa Cost | Ideal Down Payment |

| ₹75 Lakhs | ₹10–15 Lakhs |

| ₹1 Crore | ₹15–25 Lakhs |

| ₹1.5 Crores | ₹25–40 Lakhs |

| ₹2 Crores | ₹40–50 Lakhs |

A larger down payment offers several advantages:

- Lower EMI

- Lower interest burden

- Faster loan approval

- Better financial flexibility

Personally, I always suggest aiming for at least 20% of the villa cost before beginning your search.

Your future self will thank you every month when the EMI arrives.

Home Loan Eligibility for IT Employees in Hyderabad

Hyderabad’s villa market is heavily driven by IT professionals.

Companies in HITEC City, Gachibowli, Financial District, and Nanakramguda continue to create strong demand for premium housing.

Fortunately, IT employees often enjoy:

- Stable income profiles

- Faster loan approvals

- Higher loan eligibility

- Competitive interest rates

Many lenders view experienced software engineers, managers, and technology professionals as low-risk borrowers.

If you’re working in the IT sector and earning above ₹1.5 lakh per month, your chances of qualifying for villa financing improve significantly.

Financial Planning for First-Time Villa Buyers in Hyderabad

Buying a villa isn’t just about getting a loan.

It’s about building a financial foundation.

Follow These Smart Steps

Build an Emergency Fund

Keep at least 6–12 months of expenses aside.

Reduce Existing Debt

Clear personal loans and unnecessary credit card debt before applying.

Improve Your Credit Score

Pay bills on time and maintain healthy credit utilization.

Save for Registration Costs

Many buyers forget about:

- Registration charges

- Legal fees

- Interior expenses

- Maintenance deposits

These costs can add several lakhs to your overall budget.

Avoid Lifestyle Inflation

Just because your salary increases don’t mean every increment should go toward gadgets, vacations, and expensive coffee.

A villa fund deserves a place in your monthly budget.

Is Buying a Villa in Hyderabad a Good Investment?

This is where Hyderabad stands out.

Several infrastructure projects continue to support long-term real estate growth:

- Outer Ring Road (ORR)

- Regional Ring Road (RRR)

- Metro expansion plans

- IT corridor growth

- Aerospace and manufacturing hubs

Villa communities also offer:

- Better privacy

- More open space

- Premium lifestyle amenities

- Higher demand among family buyers

Historically, quality villa projects in growing micro-markets have shown strong appreciation potential compared to many apartment segments.

Of course, location remains everything.

A villa in a well-connected growth corridor generally performs better than one in an isolated area.

Can a Salaried Employee Buy a Villa in Hyderabad?

Absolutely.

In fact, a large percentage of villa buyers in Hyderabad today are salaried professionals.

The key is balancing:

- Salary

- Savings

- Down payment

- Loan eligibility

- Long-term financial goals

You don’t necessarily need a ₹5 lakh monthly salary to own a villa.

Many buyers successfully purchase villas with household incomes ranging from ₹1.5 lakh to ₹3 lakh per month through careful planning and joint financing.

The dream is not reserved only for business owners or ultra-high-net-worth individuals.

Frequently Asked Questions (FAQs)

For villas priced between ₹75 lakhs and ₹1.5 crores, a monthly salary between ₹1 lakh and ₹2 lakh is generally considered suitable, depending on your down payment and existing financial commitments.

Yes. With sufficient savings for a down payment and good home loan eligibility, buying a villa in the ₹70–80 lakh range may be possible.

A person earning ₹1 lakh monthly may qualify for approximately ₹50–60 lakhs, while someone earning ₹2 lakhs monthly could be eligible for around ₹1 crore or more.

A down payment of at least 20% of the property value is generally recommended.

Hyderabad continues to be one of India’s strongest real estate markets, supported by IT growth, infrastructure development, and increasing demand for premium housing.

IT professionals often benefit from stable income profiles and may qualify for higher loan amounts and competitive interest rates.

Focus on building savings, improving your credit score, reducing debt, creating an emergency fund, and preparing for additional purchase costs beyond the villa price.

Final Thoughts

So, how much salary is needed to buy a villa in Hyderabad?

For most buyers, a monthly income between ₹1.5 lakh and ₹3 lakh offers a comfortable path toward villa ownership. However, your salary is only one piece of the puzzle.

Strong savings, a healthy credit score, smart financial planning, and the right location choice can make a huge difference.

Hyderabad continues to attract ambitious professionals looking for a better lifestyle, more space, and long-term wealth creation through real estate.

If you’ve been wondering whether villa ownership is possible, now might be the perfect time to start planning. The dream villa may be closer than you think.

Ready to explore villa projects in Hyderabad? Start by calculating your budget, checking your loan eligibility, and speaking with trusted real estate experts who can guide you toward the right investment.

{kind=link}